Form 4797 Sales of Business Property

Introduction

Form 4797, Sales of Business Property is a supplemental form used by businesses to report the sale, exchange, or involuntary conversion of business property and assets.

For organizations filing IRS Form 990-T, Form 4797 is important for reporting gains or losses from business property that may impact unrelated business taxable income (UBTI).

In this resource article, we will help you understand Form 4797 by clarifying who must file, the filing requirements, and addressing commonly asked questions.

Table of Contents

What is Form 4797?

Form 4797 is used by businesses and individuals to report the sale, exchange, or involuntary conversion of property used in a trade or business. This can include Real estate , Machinery vehicles , and Other assets that have been depreciated or amortized.

The form captures detailed information about the transaction, including the original cost of the property, accumulated depreciation, and the sales price, to determine the gain or loss on the sale.

Who must file Form 4797?

Form 4797 must be filed by taxpayers who sell, exchange, or otherwise dispose of property used in a trade or business. This may include:

- Individuals and sole proprietors

- Partnerships

- Corporations

- S corporations

- Tax-exempt organizations

You may also need to file Form 4797 if:

- You sell business property, such as equipment, machinery, vehicles, or buildings.

- You dispose of depreciable or amortizable business assets.

- Your property was involuntarily converted due to theft, casualty, destruction, or condemnation.

- You are filing Form 990-T and disposing of property connected to unrelated business income activities

Choose TaxZerone for a filing experience that goes beyond expectations.

Empower your tax compliance journey with us today!

How to Complete Form 4797: Line-by-Line Instructions

In Form 4797, enter the taxpayer’s name and identifying number, such as an SSN or EIN, exactly as shown on the tax return. This will help the IRS identify and process the form properly.

When a partnership or S corporation disposes of Section 179 property, each partner or shareholder must report their share of the transaction using the appropriate IRS forms.

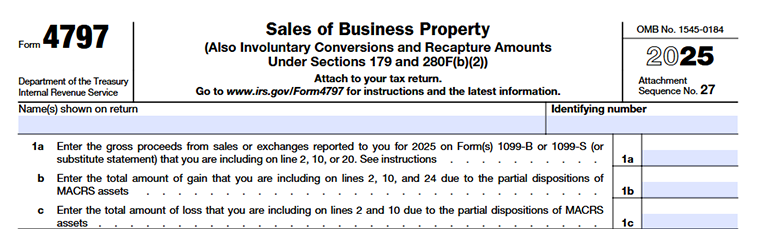

Line 1a

Report total gross proceeds from sales or exchanges reported on Forms 1099-S or 1099-B that are included on Form 4797.

Line 1b

Enter the total amount of gains from partial dispositions of MACRS property.

Line 1c

Enter the total amount of losses from partial dispositions of MACRS property.

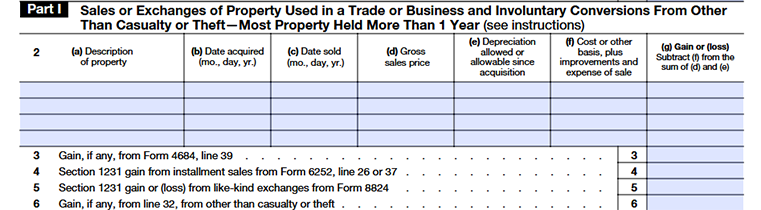

Part I - Sales or Exchanges of Property Used in a Trade or Business and Involuntary Conversions from Other Than Casualty or Theft-Most Property Held More Than 1 Year

Part I of Form 4797 is used to report Section 1231 transactions related to business property held for more than one year. It usually encompasses the sale, exchange, or involuntary conversion of assets of the trade or business, such as real estate, depreciable property, livestock for use in a trade or business, timber, and some crops.

But it does not include items such as inventory held for sale, copyrights, patents, artistic works, and government publications in section 1231.

Line 2

Line 2 is used to report details of each property transaction:

Column (a)

Description of the property sold or exchanged.

Column (b)

Enter the date the property was acquired. If the property was inherited, enter “Inherited” instead of the acquisition date.

Column (c)

Date the property was sold or disposed of.

Column (d)

Gross sales price of the property.

Column (e)

Enter the total depreciation allowed or allowable on the property since it was acquired. This includes depreciation deductions claimed or that could have been claimed during the ownership period.

Column (f)

Enter the original cost or other basis of the property, along with improvements made and any selling expenses related to the disposition of the property.

Column (g)

Enter the gain or loss from the transaction after adjusting basis and depreciation.

Line 3

Enter gains reported from Form 4684 related to casualty or theft transactions in Line 39.

Line 4

Report Section 1231 gains from installment sales reported on Form 6252 in line 26 or Line 37.

Line 5

Enter gains or losses from like-kind exchanges reported on Form 8824.

Line 6

Report gains if any from Line 32 and from other involuntary conversions not related to casualty or theft.

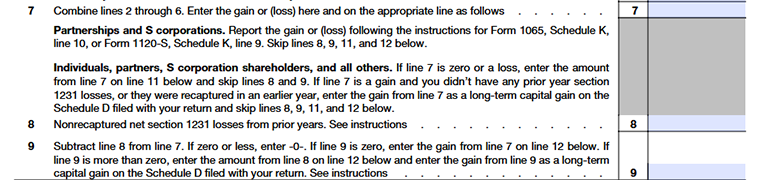

Line 7

Combine the amounts from lines 2 through 6 and enter the total gain or loss. Partnerships and S corporations must report the amount according to the instructions for IRS Form 1065 or Form 1120-S (Schedule K-1) and can skip lines 8, 9, 11, and 12.

Individuals, partners, S corporation shareholders, and other filers should follow these rules:

- If line 7 shows a loss or zero, enter the amount on line 11 and skip lines 8 and 9.

- If line 7 shows a gain and there are no prior unrecaptured Section 1231 losses, the gain is generally reported as a long-term capital gain on Schedule D (1120-S).

- If there are prior year unrecaptured Section 1231 losses, continue to lines 8 and 9 to determine how the gain should be treated.

Line 8

Enter any Non recaptured Section 1231 losses from the previous five tax years. These are prior year Section 1231 losses that have not yet been offset against current Section 1231 gains. Current year gains may be treated as ordinary income up to the amount of these unrecaptured losses.

Line 9

Line 9 is used to determine whether any prior year of Section 1231 losses still remain to be recaptured.

- If line 9 is zero, the entire gain reported on line 7 is treated as a recaptured Section 1231 loss for the current tax year.

- If line 9 is greater than zero, it means that all prior-year non -recaptured Section 1231 losses have been fully recaptured. In this case, enter the amount from line 8 on line 12, and report the remaining gain from line 9 as a long-term capital gain on Schedule D.

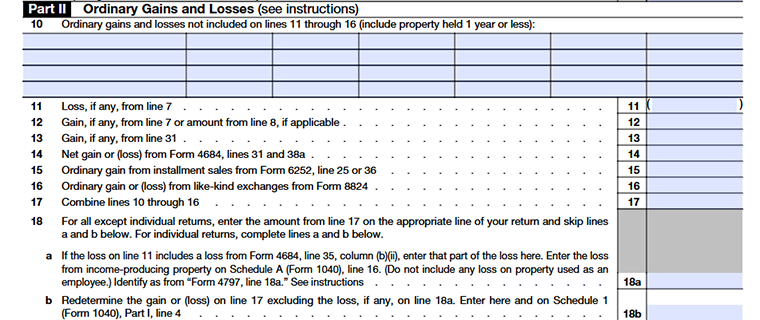

Part II - Ordinary Gains and Losses

Part II of IRS Form 4797 is utilized to disclose gains and losses that cannot be accounted for using either Part I or Part III. This particular section is usually applied to property that was acquired within one year or less and some business transactions.

Line 10

Report ordinary gains and losses that are not included on lines 11 through 16. This may include:

- Property held for one year or less

- Losses from abandoned business or investment property

- Income from property deducted under the de minimis safe harbor rule

- Gains or losses from securities or commodities under the mark-to-market election

- Deferred gains from qualifying electric transmission property

- Losses from Small Business Investment Company (SBIC) stock

- Losses from Section 1244 small business stock

- Certain preferred stock transactions

Line 11

Enter any loss amount carried over from line 7.

Line 12

Enter gains from line 7 or line 8 that must be treated as ordinary income.

Line 13

Report gains from casualty or theft transactions from Form 4684, line 31.

Line 14

Enter net gains or losses reported from Form 4684, line 31 and line 38a.

Line 15

Report ordinary gains from installment sales reported on Form 6252, line 25 and line 36.

Line 16

Enter ordinary gains or losses from like-kind exchanges reported on Form 8824.

Line 17

Combine lines 10 through 16 and enter the total ordinary gain or loss.

Line 18

For individual tax returns, complete lines 18a and 18b to determine the correct treatment of gains and losses reported in Part II.

Line 18a

Complete line 18a if there is a gain on Form 4797, line 3 , a loss on Form 4797, line 11, and a loss on Form 4684, line 35, column (b)(ii). Enter the smaller of the two losses from Form 4797, line 11, or Form 4684, line 35, column (b)(ii), treating both amounts as positive numbers for comparison purposes.

Report the loss from income-producing property on Schedule A (Form 1040), line 16, and identify it as “Form 4797, line 18a.” Do not include losses related to employee-use property.

Line 18b

Recalculate the gain or loss from line 17 after excluding any loss entered on line 18a. Enter the updated amount on line 18b and report it on Schedule 1 (Form 1040), Part I, line 4.

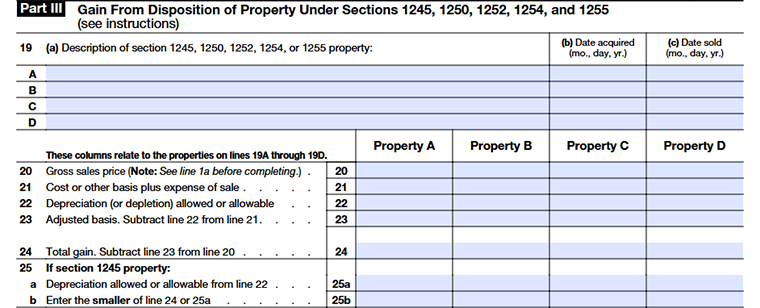

Part III - Gain from Disposition of Property Under Sections 1245, 1250, 1252, 1254, and 1255

Depreciation recapture and any other gains that need to be reported as ordinary income upon the sale or other disposition of specific business assets can be calculated using Part III of Form 4797. Property held for one year or less is generally reported in Part II instead of Part III.

Line 19

Line 19 is used to enter details about property disposed of under Sections 1245, 1250, 1252, 1254, or 1255.

Column (a)

Enter a description of the property sold or disposed of.

Column (b)

Enter the date the property was acquired.

Column (c)

Enter the date the property was sold or disposed of.

Line 20

Enter the total consideration for the transfer of the property, including any cash, FMV of property acquired, and mortgage or indebtedness assumed by the purchaser.

In casualty or theft transactions, enter any insurance payments you have received or anticipate receiving, regardless of whether a claim has been filed.

For property held under Section 1255:

- If the property was sold or exchanged, enter the amount realized.

- If the property was disposed of in any other manner, enter the FMV of the property.

Line 21

Enter the adjusted cost or basis of the property after reducing it for certain credits, such as the enhanced oil recovery credit or disabled access credit. Do not reduce the basis for items already included in line 22 calculations.

Line 22

Line 22 is used to calculate total depreciation, amortization, and other deductions previously claimed for the property.

- Add all applicable deductions and basis reductions

- From the above total, subtract any applicable recapture amounts or basis increases

Additional depreciation adjustments may also be required if another asset's adjusted basis was used to determine the basis of the property reported on line 19.

Line 23

Enter the adjusted basis of the property by subtracting line 22 from line 21. For Section 1255 property, enter the adjusted basis of the Section 126 property disposed of.

Line 24

Subtract line 23 from line 20 to calculate the total gain from the property disposition.

Line 25a

Enter the total depreciation or amortization allowed or allowable for the Section 1245 property reported on line 19. This may include depreciation deductions, Section 179 expense deductions, amortization, and certain other deductions previously claimed for the property.

Section 1245 property generally includes depreciable personal property, certain business equipment, machinery, storage facilities, and specific real property used in business activities.

Line 25b

Enter the smaller of line 24 or line 25a. This amount is generally treated as ordinary income under the Section 1245 depreciation recapture rules.

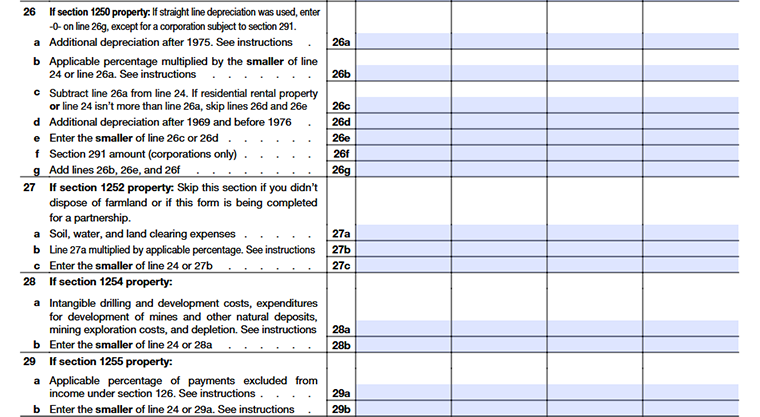

Line 26

This line pertains to Section 1250 property that normally covers real property like buildings. If straight-line depreciation was used, line 26g is generally entered as zero unless special corporate recapture rules apply.

Line 26a

Enter the additional depreciation claimed after 1975. Additional depreciation is the amount by which actual depreciation, including any special depreciation allowance or commercial revitalization deduction, exceeds the depreciation calculated using the straight-line method.

Line 26b

In most cases, use 100% as the applicable percentage for this line. However, different percentages may apply for certain low-income rental housing properties under Section 1250(a)(1)(B) rules.

Line 26c

Subtract line 26a from line 24 to calculate the balance amount. If the property is residential rental property, or if line 24 is not greater than line 26a, skip lines 26d and 26e.

Line 26d

Enter additional depreciation claimed after 1969 and before 1976.

Line 26e

Enter the smaller amount from line 26c or line 26d.

Line 26f

Corporations subject to Section 291 must report 20% of the excess amount that would have been treated as ordinary income if the property were considered Section 1245 property instead of Section 1250 property. If straight-line depreciation was used, the ordinary income amount is generally 20% of the Section 1245 recapture amount.

Line 26g

Add lines 26b, 26e, and 26f to determine the total Section 1250 recapture amount.

Line 27

Line 27 applies to Section 1252 property, generally involving certain farmland where soil and water conservation or land clearing expenses were previously deducted. Partnerships generally do not complete this section. Instead, partners must report Section 1252 amounts based on the information provided by the partnership.

Line 27a

Enter deductible soil, water, and land clearing expenses related to the property.

Line 27b

Multiply line 27a with the applicable percentage.

Line 27c

Enter the smaller amount from line 24 or line 27b.

Line 28

Line 28 applies to Section 1254 property related to oil, gas, geothermal, mining, and natural resource properties.

Line 28a

Line 28a applies to Section 1254 property, including oil, gas, geothermal, mining, and other natural resource properties. Enter the total deductible costs previously claimed that reduced the property’s adjusted basis.

- For property placed in service before 1987, include intangible drilling and development costs deducted after 1975 that would otherwise have been added to the property’s basis.

- For property placed in service after 1986, include deductions claimed under Sections 263, 616, or 617, along with depletion deductions under Section 611 that reduced the property’s adjusted basis.

If only part of the Section 1254 property or a partial ownership interest was disposed of, special Section 1254 rules may apply.

Line 28b

Enter the smaller amount from line 24 or line 28a.

Line 29

Line 29 applies to Section 1255 property involving payments previously excluded from income under Section 126.

Line 29a

Use 100% if the property is disposed of less than 10 years after receiving payments excluded from income. After the 10-year period, reduce the percentage by 10% for each additional year or partial year the property was held. If the property was held for 20 years or more, use zero.

Line 29b

If part of the gain on line 24 is already treated as ordinary income under Sections 1231 through 1254, enter the smaller of:

- Line 24 reduced by the gain already treated as ordinary income under another section, or

- The amount from line 29a.

Line 30

Enter the total gains for all properties reported in Part III after completing the calculations for each property column.

Line 31

Add the amounts from columns A through D for lines 25b, 26g, 27c, 28b, and 29b. Enter the total on line 31 and report it on line 13.

Line 32

Subtract line 31 from line 30. Enter the portion related to casualty or theft from Form 4684 on line 33. Enter the remaining amount from other transactions on Form 4797, line 6.

Part IV - Recapture Amounts Under Sections 179 and 280F(b)(2) When Business Use Drops to 50% or Less

Column (a)

Complete column (a) if you claimed a Section 179 deduction for property placed in service after 1986 and the business use dropped to 50% or less during the tax year.

Column (b)

Complete column (b) for listed property, such as certain vehicles or business-use assets, if the business use decreased to 50% or less during the year.

If multiple properties are subject to recapture, calculate each one separately and attach the details to the tax return.

Line 33

- Column (a) – Enter the Section 179 deduction originally claimed for the property.

- Column (b) – Enter the depreciation allowed in prior years, including any Section 179 deduction claimed.

Line 34

- Column (a) – Enter the depreciation that would have been allowed from the year the property was placed in service through the current year.

- Column (b) – Enter the depreciation that would have been allowed if the property had not been used more than 50% for business purposes.

Line 35

Subtract line 34 from line 33 to determine the recapture amount. Report this amount as other income on the same form or schedule where the original deduction was claimed.

If the property was used for both business and income-producing purposes, part of the recapture amount may also be subject to self-employment tax. Increase the property’s basis by the recapture amount reported.

Commonly Asked Questions

1. What is the difference between a short-term gain and a long-term gain on the sale of business property?

2. What types of property are reported on Form 4797?

Form 4797 is used to report the sale or exchange of business property, which includes real estate, machinery, equipment, vehicles, and other assets that have been used in a trade or business and have been depreciated or amortized. It also covers involuntary conversions, such as property destroyed by casualty or condemned.

3. Do I need to file Form 4797 if I sell a business asset that is part of a Section 1231 transaction?

4. What Is the Difference Between Form 8949 and Form 4797?

- Form 8949 is used to report sales of investment assets such as stocks, bonds, and cryptocurrency and

- Form 4797 is used to report the sale or disposal of business property such as equipment, machinery, and rental property.