If your organization or trust sold investments during the year, you may need to file IRS Form 8949. This form provides detailed reporting of capital asset transactions before totals are transferred to IRS Schedule D.

Whether you are reviewing form 8949 information, checking the latest form 8949 instructions 2025, or understanding how IRS Form 8949 and Schedule D work together, it’s important to know that this form ensures every sale is properly documented.

For exempt organizations and trusts, IRS tax Form 8949 is commonly required when:

- When capital gains become taxable under Unrelated Business Taxable Income reported on Form 990-T

- A split-interest trust reports investment transactions as part of its annual filing on Form 5227

- Brokerage 1099-B statements must be reconciled

- Adjustments to cost basis are necessary

In short, Form 8949 IRS reporting provides transaction-level transparency, while IRS Schedule D summarizes totals for final reporting.

What’s New in Form 8949?

Understanding the latest updates can help you report your transactions accurately. Here’s what you need to know:

How should you report digital asset transactions?

| Transaction Type | Boxes to Use | Form Section | Do Not Use |

|---|---|---|---|

| Short-term digital asset transactions | Boxes G, H, or I | Part I of Form 8949 | Box C |

| Long-term digital asset transactions | Boxes J, K, or L | Part II of Form 8949 | Box F |

We explain the purpose and usage of each box in detail in the section below to help you select the correct option.

Table of Contents

What is IRS Form 8949?

IRS tax Form 8949 is used to report detailed sales and exchanges of capital assets. Instead of listing only totals, the IRS requires each transaction to be disclosed separately unless it qualifies for summary reporting.

Capital Assets Reported on Form 8949

Capital assets generally include property held for investment or certain business-related purposes. Examples of such assets include:

- Stocks and bonds

- Real estate

- Cryptocurrency and digital assets

- Partnership interests

- Other investment assets

In addition to standard asset sales, Form 8949 is utilized to report transactions that require specific or special tax treatment, including the following:

- Capital losses, nondeductible losses, and losses from wash sales.

- Short sales

- Traders in securities reporting

- Gain or loss from options

- Installment sales

- Demutualization of life insurance companies

- Exclusion or rollover of gain from qualified small business (QSB) stock

- Other rollover transactions

- Deferral of gain invested in a Qualified Opportunity Fund (QOF)

- Special reporting situations for corporations, partnerships, estates, and trusts

These special situations do not change what a capital asset is - but they affect how the transaction is reported on IRS Form 8949.

Who must file IRS Form 8949?

You must file Form 8949 IRS if:

- You sold or exchanged a capital asset

- You received Form 1099-B

- You need to adjust cost basis

- Your brokerage did not report basis to the IRS

- Schedule D requires transaction detail

This applies to:

- Individuals

- Corporations

- Estates

- Trusts

- Tax-exempt organizations with taxable activity

Even exempt entities may need IRS Form 8949 and Schedule D when reporting taxable capital gains.

Choose TaxZerone - Your Gateway to Seamless Tax Filing

Complete your Form 990-T return and 8949 filing requirements with ease!

Why attach Form 8949 to Form 990-T?

Organizations filing IRS Form 990-T report Unrelated Business Taxable Income (UBTI). When capital gains are connected to unrelated trade or business activity, IRS tax Form 8949 may be required.

Common Situations

- Sale of property used in unrelated business

- Sale of partnership interest generating UBTI

- Disposition of unrelated business assets

The form 8949 instructions 2025 clarify that detailed reporting must occur before completing certain Schedule D totals.

Why attach Form 8949 to Form 5227?

Split-interest trusts filing IRS Form 5227 frequently report investment activity. Because these trusts often sell securities during the year, Form 8949 IRS reporting ensures each transaction is properly documented.

Why it matters

- Tracks short-term vs long-term gains

- Supports Schedule D calculations

- Ensures proper income tier classification

- Provides transparency for trust reporting

For many trusts, IRS Form 8949 and Schedule D are used together annually.

How to file Form 8949 with TaxZerone?

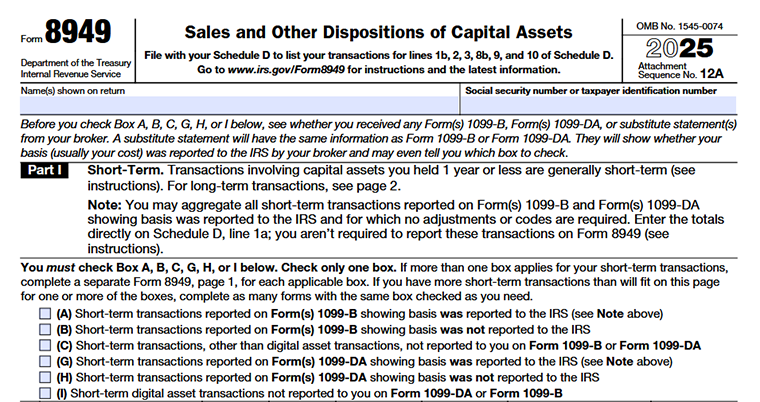

Part I - Short-Term

Short-Term Capital Gains and Losses

- A short-term capital gain or loss occurs when you sell or dispose of a capital asset that you held for one year or less. The holding period begins the day after you acquire the property and includes the day you sell or dispose of it.

- Short-term transactions must generally be reported in Part I of Form 8949. Each sale or exchange of a capital asset-such as stocks, bonds, or other investments- is listed here with details like the purchase date, sale date, proceeds, and cost basis.

- In some cases, you may not need to list each transaction on Form 8949. If the transaction meets certain IRS exceptions, it can be reported directly on line 1a of Schedule Dinstead.

- There are also special situations to keep in mind. For example, a non-business bad debt is treated as a short-term capital loss, even if the debt existed for more than one year.

Selecting the Correct Reporting Box for Short-Term Transactions

Before entering transaction details in Part I of Form 8949, you must select the correct reporting category by checking one box at the top of the form. These boxes help the IRS understand how your transaction was reported to you and whether the cost basis information was also reported to the IRS.

Important:

- Check only one box that best describes your short-term transactions.

- If your transactions fall under more than one category, you must complete a separate Form 8949 for each applicable box.

- If you have more transactions than can fit on one page, you may attach additional copies of Form 8949 with the same box checked.

Box Options for Short-Term Transactions

Box A - Basis Reported to the IRS

Check Box A if your short-term transactions were reported to you on Form 1099-B, and the cost basis was also reported to the IRS.

Box B - Basis Not Reported to the IRS

Check Box B if you received Form 1099-B, but the cost basis was not reported to the IRS. In this case, you must provide the cost basis when reporting the transaction.

Box C - Transactions Not Reported on Form 1099

Check Box C if the short-term transaction was not reported to you on Form 1099-B or a digital asset form. You still need to report the transaction using your own records.

Box G - Digital Asset Transactions with Basis Reported

Check Box G if your digital asset transactions were reported on Form 1099-DA, and the cost basis was reported to the IRS.

Box H - Digital Asset Transactions with Basis Not Reported

Check Box H if your digital asset transactions were reported on Form 1099-DA, but the cost basis was not reported to the IRS.

Box I - Digital Asset Transactions Not Reported

Check Box I if you had short-term digital asset transactions that were not reported to you on Form 1099-DA or Form 1099-B.

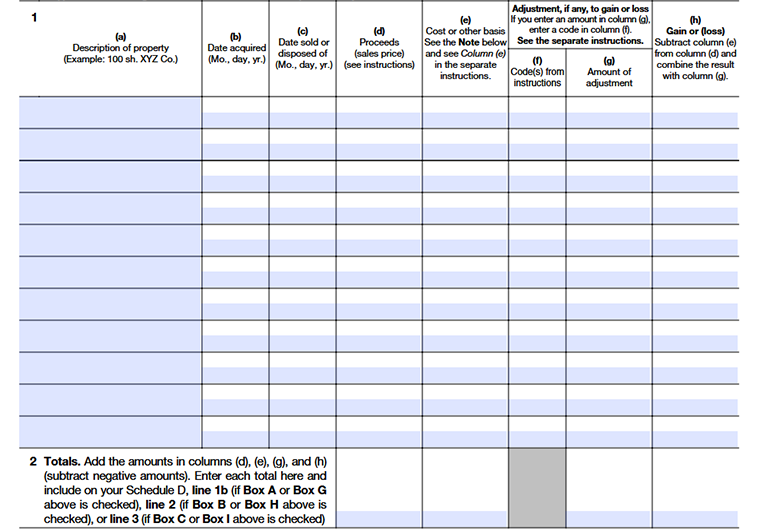

Line 1

Column (a) – Description of Property

Enter a clear description of what you sold. Include:

- Number of shares (for stocks)

- Stock ticker symbol (optional but recommended)

- Full name or symbol of digital asset

- Exact quantity sold

Column (b) – Date Acquired

Enter the date you originally purchased or acquired the asset. Special cases:

- If purchased on multiple dates → Enter “VARIOUS”

- If inherited → Enter “INHERITED”

- For exchange-traded assets → Use the trade date

This date determines whether your transaction qualifies as short-term or long-term.

Column (c) – Date Sold or Disposed Of

Enter the actual sale date. The IRS uses this date to confirm:

- The tax year of the sale

- Holding period classification

Column (d) – Proceeds

Enter the gross amount received from the sale.

- Use the number shown on Form 1099-B or 1099-DA.

- Do not subtract fees unless already adjusted.

Column (e) – Cost or Other Basis

Enter what you originally paid for the asset, including:

- Purchase price

- Commissions

- Transaction fees

Accurate basis reporting prevents overpaying taxes.

Column (f) – Codes from instructions

Enter adjustment codes if needed. Common reasons:

- Wash sale adjustments

- Incorrect basis correction

- Special exclusions

If no adjustment applies, leave blank.

Column (g) – Adjustment Amount

If you entered a code in Column (f), enter the adjustment amount here.

- Negative numbers go in parentheses.

- This modifies your gain or loss calculation.

Column (h) – Gain or (Loss)

This column calculates your result:

Proceeds (d) – Cost Basis (e) ± Adjustment (g) = Gain or Loss

If positive → Gain

If negative → Loss

These totals flow to Schedule D, where your final capital gain tax is determined.

Line 2

Line 2 of Form 8949 helps reconcile your total capital gains or losses with what you report on Schedule D (Form 1040). First, add all amounts in Column (h) from your Forms 8949 based on the box you checked. Then, ensure the totals match the corresponding amounts on Schedule D.

- If you checked Box A or Box G, the total should match the combined amounts of columns (d), (e), and (g) on Schedule D, Line 1b.

- If you checked Box E or Box K, the total should match the combined amounts of columns (d), (e), and (g) on Schedule D, Line 9.

Example: Adjustment

If your sales price (Column d) is $6,000, your cost basis (Column e) is $2,000, and you have a ($1,000) adjustment in Column (g):

$6,000 − $2,000 = $4,000

$4,000 − $1,000 = $3,000 gain

Enter $3,000 in Column (h).

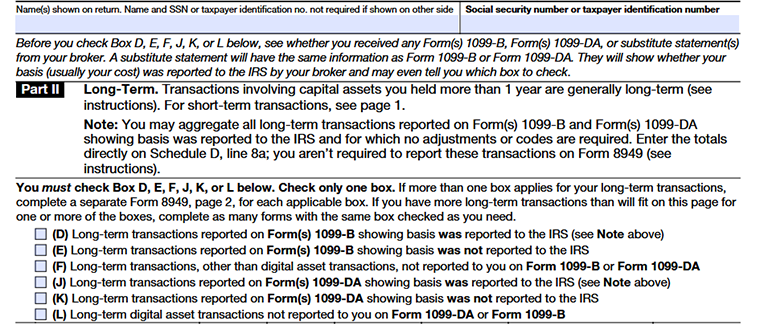

Part II - Long-Term

Long-Term Capital Gains and Losses

- A long-term capital gain or loss applies when you sell or dispose of a capital asset that you held for more than one year. Like short-term transactions, the holding period begins the day after the asset is acquired and includes the day it is sold.

- These transactions are reported in Part II of Form 8949. Long-term transactions often receive different tax treatments, so separating them from short-term transactions is an important step when preparing your tax return.

- In certain situations, you may be able to report the transaction directly on line 8a of Schedule D instead of listing each transaction on Form 8949.

- Another important rule involves inherited property. When you sell property received through inheritance, the IRS generally treats the transaction as long-term, regardless of how long you actually held the asset before selling it.

Box Options for Long-Term Transactions

Box D - Basis Reported to the IRS

Select Box D if your long-term transactions were reported on Form 1099-B and the cost basis was also reported to the IRS.

Box E - Basis Not Reported to the IRS

Select Box E if you received Form 1099-B, but the cost basis was not reported to the IRS. You will need to provide that information when completing the form.

Box F - Transactions Not Reported on Form 1099

Select Box F if your long-term transactions (other than digital assets) were not reported on Form 1099-B or Form 1099-DA.

Box J - Digital Asset Transactions with Basis Reported

Select Box J if your digital asset transactions were reported on Form 1099-DA and the cost basis was reported to the IRS.

Box K - Digital Asset Transactions with Basis Not Reported

Select Box K if your digital asset transactions were reported on Form 1099-DA, but the cost basis was not reported to the IRS.

Box L - Digital Asset Transactions Not Reported

Select Box L if you had long-term digital asset transactions that were not reported to you on Form 1099-DA or Form 1099-B.

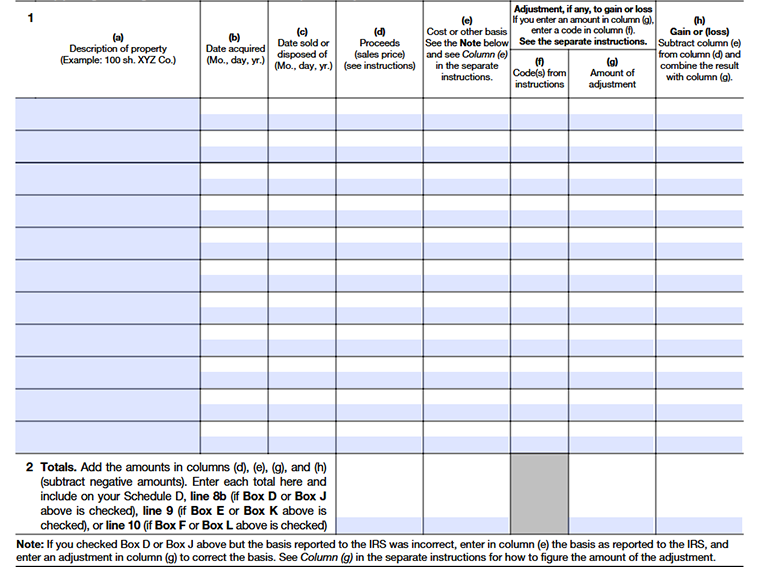

Line 1 has already been explained in Part I above. If you need additional clarification about how to complete this line or understand the reporting requirements, please refer to Part I of IRS Form 8949, where the instructions and examples are provided in detail.

Line 2

Line 2 is used to calculate the total amounts for the transactions listed on this page.

Add the amounts from Column (d) Proceeds, Column (e) Cost or Other Basis, Column (g) Adjustments, and Column (h) Gain or Loss. While adding the values, make sure to subtract any negative amounts.

After calculating the totals, enter each column total on Line 2 and transfer the appropriate amount to Schedule D (Form 1040):

- Line 8b – If Box D or Box J is checked

- Line 9 – If Box E or Box K is checked

- Line 10 – If Box F or Box L is checked

Commonly Asked Questions

1. How do I know if I need to file Form 8949?

2. What is the difference between short-term and long-term transactions on Form 8949?

Short-term transactions involve assets held for one year or less, while long-term transactions involve assets held for more than one year. These are reported separately on Form 8949 because they are subject to different tax rates.